Now we have a uniformly speculative and even slightly conservative thought: take steel company Commercial Metals (NYSE: cc), to earn income by increasing the purchasing power of his products.

Growth potential and duration : 10,5 % during 14 Months.

Why stocks can go up: US industrial boom.

How do we act: we take at the moment 31,17 $.

No guarantees

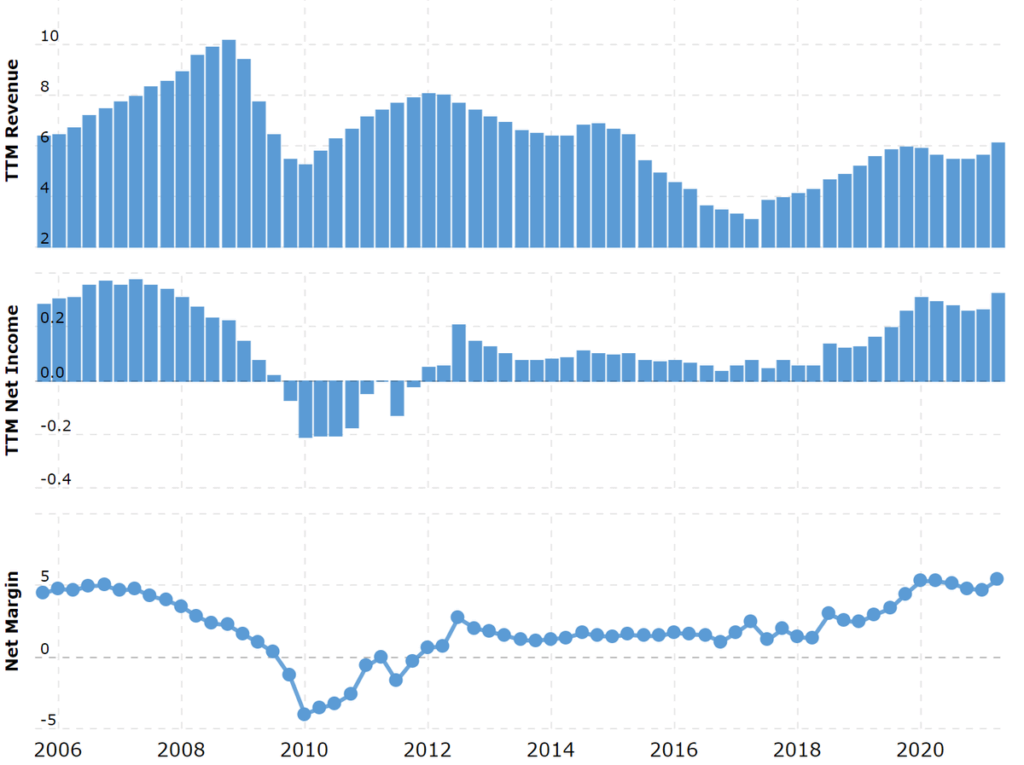

And what is there with the author's forecasts

What the company makes money on

CMC is engaged in the creation and processing of steel products. In accordance with the annual report, its revenue is distributed by type of product in the following way:

- Raw steel products - 13,29 %. Scrap metal from the organization's own landfills for future processing and use by other steel organizations.

- Steel products - 41,73 %. Iron roof, iron beams, reinforcing steel and mounting fasteners. Products for industrial companies, agricultural production and petrochemical industry.

- Recycled steel products - 37,65 %. Iron plates, iron coils, iron rods, skates, rolls of bar steel. Products for the construction industry for the construction of powerful buildings.

- Other - 7,33 %. Rental of company equipment for the construction industry and the creation of steel products specifically for a number of industries: heavy truck manufacturers, energy companies and military equipment.

Geographic distribution of the company's revenue:

- North America - 87,09%. Companies, which is located in the USA. Sector Adjusted EBITDA — 13,86 % from its proceeds.

- Europe - 12,91 %. CMC factories in Poland. Sector Adjusted EBITDA — 8,86 % from its proceeds.

Distribution of revenue by country:

- USA - 83,3 %.

- Poland - ten percent.

- China —1.4 %.

- Germany - 1,2 %.

- The rest of the states 4,1 %.

Based on the only data available to us in 2019, the structure of the company's revenue by the final industries for the use of its products looks like this:

- A complex of infrastructure facilities - thirty-seven percent.

- Non-residential property - thirty-two percent.

- Residential real estate - sixteen percent.

- Equipment manufacturers and agricultural production - fifteen percent.

Arguments in favor of the company

American strong. In the idea for Emerson Electric we mentioned, that in the United States, production indicators are growing and enterprises are planning to invest in the renewal of fixed assets, - from this should fall and CMC. Moreover, many steel mills in the United States deliberately do not start up previously shut down plants., to keep high prices for steel products. And in the conditions of an industrial boom and consumer activity, manufacturers have no other choice, except how to buy that, what is.

Well, for that matter, in the second most important market for the company, Poland, everything is fine too: production figures in this country are growing, indicating an increase in orders for CMC in this country.

Price. Company P / E 11,56 and capitalization 3,76 billion dollars - a combination of these factors can lead to a rapid and tangible growth in quotations due to the influx of investors.

Purchase opportunity. The advantages mentioned above would be enough, to attract a buyer to the CMC, but there is one more thing. In numerous presentations, the company talks a lot about, how it is actively investing in the reorientation of its production facilities to the production of high value-added steel products, and indeed it is. US steel companies do not have high bottom line margins, so buying a compact and efficient CMC can be a great addition to any larger enterprise.

What can get in the way

What's next is unclear. The pandemic and the rise in crime provoked an exodus of the population from major US cities, which led to a fall in the budgets of municipalities. It follows from this, that less money will now be spent on investments in cities. This trend may have a negative impact on CMC orders in the medium term.. Or maybe not affect: in the last quarter, sales increased in all segments. However, if you look at the segment in 9 Months, ended 31 May, then in the segment “Recycled steel products” sales fell by 5,45% compared to the same period a year earlier. May be, this is a seasonal bug, but if not, it is better to be mentally prepared for negative reporting.

"You worked at the foundry, means, you're used to the heat". American steel companies now have the ability to break such prices, because foreign industrial enterprises are also increasing their demand for steel, loading steel companies outside the US with orders. There are not as many dumping opportunities for non-US steel mills now as due to the mentioned demand at home., so and therefore, that not all factories are out of quarantine. But if the dumping of non-American steel workers resumes - and not too long ago it was a big problem in the US, - then CMC marginality will suffer.

Wrecked. The company pays 0,48 $ dividends per share per year - with the current share price it turns out 1,53% per annum. It's not that big money, so that this factor helps to pump up quotes at the expense of fans of "divas", but problems are possible. The company spends heavily on upgrading its factories: plans to spend $200-225 million this year, average annual requirements to maintain the current level of operations - $150 million. The company spends about 54 million per year, which is approximately 16,36% from its profits over the past 12 Months. Basically, The company must have enough money for everything: on 2,234 billion in arrears, 853,367 million of which must be repaid during the year, the company has 443.12 million in accounts and 1,073 billion of counterparties' debts.

But, taking into account the extensive investment program of the company, there is a possibility of a reduction in payments - and from this the shares may fall.

What's the bottom line?

We take shares now by 31,17 $. Think, that the positive points indicated in the idea will contribute to the growth of these shares to 34,5 $ during the next 14 Months.