Today we have a moderately speculative idea with a conservative touch: take stock of German chemical giant BASF (ETR: LOW), to capitalize on the industrial boom in the world.

Growth potential and validity: 11,5% behind 14 months excluding dividends; 35% during 3 years excluding dividends; 8% per annum during 15 years including dividends.

Why stocks can go up: industrial rise in Germany and the world.

How do we act: take now 62,79 €.

When creating the material, sources were used, inaccessible to users from the Russian Federation. We hope, Do you know, what to do.

No guarantees

Our reflections are based on the analysis of the company's business and the personal experience of our investors, but remember: not a fact, that the investment idea will work like this, as we expect. Everything, what we write, are forecasts and hypotheses, not a call to action. To rely on our reflections or not – it's up to you.

If you want to be the first to know, did the investment work?, subscribe: as soon as it becomes known, we will inform.

And what is there with the author's forecasts

Research, like this and this, talk about, that the accuracy of target price predictions is low. And that's ok: there are always too many surprises on the stock exchange and accurate forecasts are rarely realized. If the situation were reversed, then funds based on computer algorithms would show results better than people, but alas, they work worse.

So we're not trying to build complex models.. The profitability forecast in the article is the author's expectations. We specify this forecast for the landmark: as with the investment idea as a whole, readers decide for themselves, it is worth trusting the author and focusing on the forecast or not.

We love, appreciate,

Investment editorial office

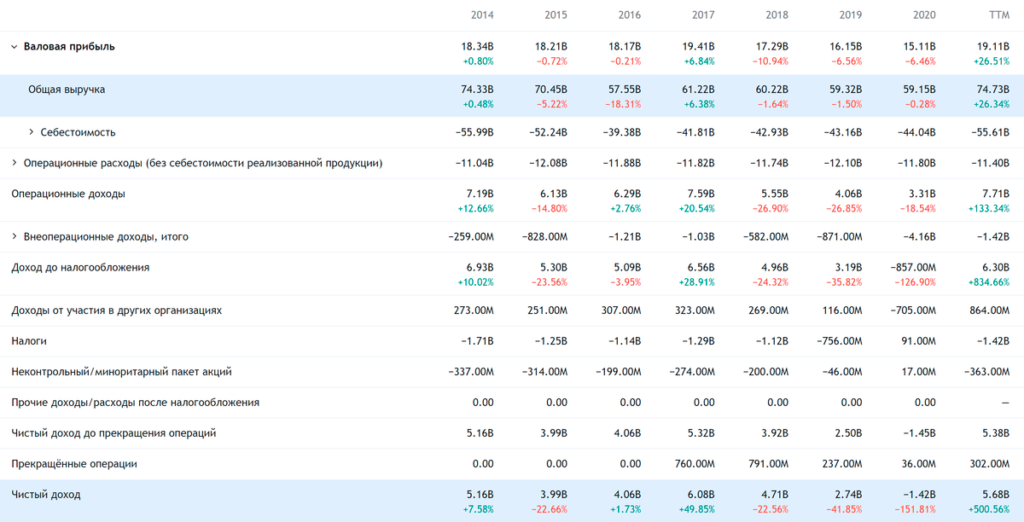

What the company makes money on

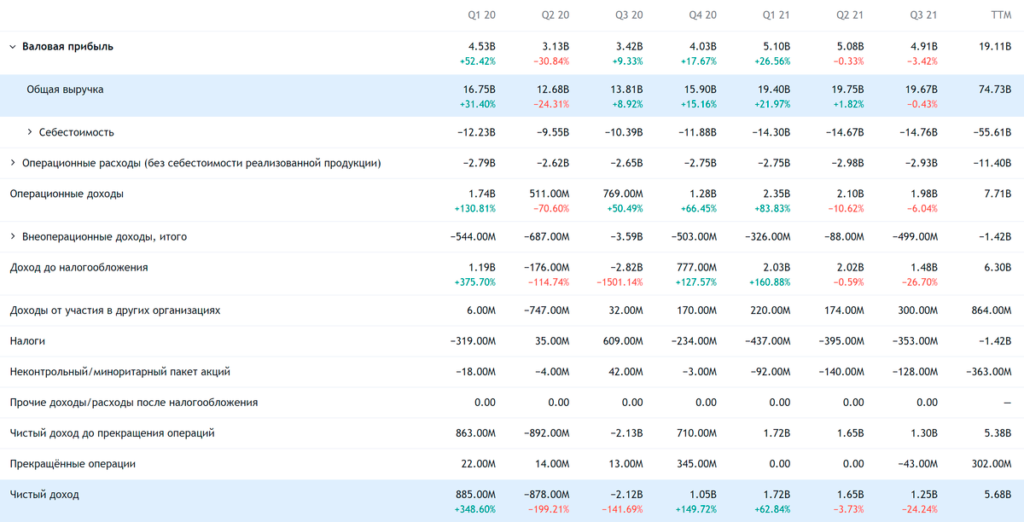

Note: since 2020 cannot be considered normal, negative or simply falling margins of many segments of the company in 2020 do not fully reflect the situation inside BASF. Therefore, next is the result of the segment in the "pre-war" 2019, to see the full picture.

According to the company's annual report, segment revenue is divided as follows.

Chemistry — 14%. These are petrochemical raw materials and precursors for the production of various types of goods.: from coatings to textiles. Segment pre-tax profit margin - minus 2,37% from its proceeds, in 2019 — 6,52%. By type of goods, segment revenue is divided as follows::

- Petrochemical materials - 67,22%.

- Precursors - 32,78%.

Materials (edit) — 18%. These are monomers and other chemical materials such as thermoplastics.. These are goods, necessary for industrial enterprises, for example for the automotive industry. Segment pre-tax profit margin - minus 1,01% from its proceeds, in 2019 — 8,48%. By type of goods, segment revenue is divided as follows::

- Polyurethanes, thermoplastic and foam — 52,48%.

- Monomers - 47,52%.

Industrial solutions — 13%. These are various coatings and chemical products both for industrial enterprises, and for the production of consumer goods. Segment pre-tax profit margin - 8,24% from its proceeds, in 2019 — 10,59%. By type of goods, segment revenue is divided as follows::

- Dispersion systems and pigments - 63,69%.

- Specialized chemical materials, made to the needs of the customer, — 36,31%.

Coating technologies — 28%. Catalysts for chemical reactions, as well as special coatings. Here, the main consumers of the company's products are industrial enterprises.. Segment pre-tax profit margin - minus 3,52% from its proceeds, in 2019 — 5,04%. By type of goods, segment revenue is divided as follows::

- Catalyst — 81,45%.

- Coatings - 18,55%.

Technology and personal care — 10%. These are solutions for perfumery and cosmetics, as well as food and pharmaceutical industries. Segment pre-tax profit margin - 11,43% from its proceeds, in 2019 — 10,6%. By type of goods, segment revenue is divided as follows::

- Care products - 66,27%. Not only cosmetics, but also cleaning agents.

- Nutrition and health - 33,73%. Taste and odor solutions for the food and perfume industry, as well as in the pharmaceutical industry and fuel production.

Agriculture solutions — 13%. These are chemical solutions for growing crops. Segment pre-tax profit margin - 7,59% from its proceeds, in 2019 — 11,87%. By type of goods, segment revenue is divided as follows::

- Fungicides - 29,59%.

- Herbicide — 32,16%.

- Insecticide — 10,77%.

- Additives to Improve Seed Growth Potential - 7,95%.

- Seeds - 19,53%.

Other — 4%. Non-core businesses of the company: oil and gas assets and chemical solutions for water and paper. Segment pre-tax profit margin - minus 50,97% from its proceeds, minus in 2019 17,87%.

Revenue by country and region:

- Europe - 41%.

- North America - 28%.

- Asian-Pacific area - 25%.

- Africa, South America and the Middle East - 6%.

Germany accounts for 17,3% the entire revenue of the company - there is no information on other countries.

Distribution of workers by country and region:

- Europe - 62,4%. Germany is 47,1% the entire workforce of the company.

- Asian-Pacific area - 16,1%.

- North America - 15,4%.

- African countries, South America and the Middle East - 6,1%.

Arguments in favor of the company

Как Covestro, only more. Last week we had an investment idea for a similar German company Covestro. The prerequisites are the same here.: industrial growth in Europe and the world. And even more: BASF is still involved in agriculture, where more activity can be expected due to food shortages and rising food prices.

The company's revenue structure is sufficiently diversified, so BASF, as the English say, "a finger in every pie". This is a plus these days., when investors seek stability.

Wrecked. The company pays 3,3 € dividend per share per year, which gives approximately 5,25% per annum. This is a lot even by American standards - and by German standards it’s just a fairy tale. I think, that supporters of the idea of that, that "money should work".

ESG. Like Covestro, BASF publishes very detailed breakdowns of ESG metrics in its reporting. And unlike Covestro, BASF's numbers don't look far-fetched.: for example, BASF's 2020 emissions increased - this could be used as an argument by eco-investors against the company. But at the same time, BASF's integrity can also play a positive role.: fewer risks of company disclosures and subsequent harassment.

Cheap. Company P / E — 10,26, a P / S — 0,76. It's very cheap, especially considering the dividend attractiveness of these shares.

What can get in the way

Such are the times. BASF does business around the world. And that means, that problems with the cost of raw materials and logistics, for example in the USA and Eurozone countries, will be a problem for the company and can have a very negative impact on its reporting.

Moreover, this effect may be indirect.: for example, shortage of semiconductors is forcing automakers to shut down factories, which reduces the demand for related BASF products. Well, let's not forget about the rise in gas prices in Europe, which is likely to have the worst effect on the company's financial statements.

Wrecked. The company spends about 3 billion euros on dividends a year - almost 52% from her profits for the past 12 Months. But the company ended 2020 with a loss, and dividends were paid at a loss to BASF - and not a fact, that history with quarantine will not repeat itself.

At the same time, the company has a lot of debts.: 25,166 bn euro non-term and 20.322 bn term debt, to be repaid within a year. She doesn't have much money.: 2,899 billion in accounts and 12.291 billion debts of counterparties.

And although BASF can “scrape together” the required amount to close urgent obligations and dividends, risks of lower business profitability due to rising costs and a new quarantine could lead to dividend cuts.

Another company can cut dividends for the sake of investing in business development. In any case, a decrease in payments will have a very bad effect on quotes in the medium term., because the idea is largely based on the dividend factor: from cutting payments, shares will fall.

Stability. Diversifying a company's business in practical terms can mean, that revenue growth in one segment can offset a decline in another. In other words, do not expect a strong growth in financial indicators here.

It is not cheap. In absolute terms, BASF is very expensive: its capitalization is approximately 57.76 billion euros. It's not a sin, but such a cost greatly offsets the effect of a possible pumping of these shares by German retail investors.

What's the bottom line?

You can take shares now by 62,79 €. And then there are three options.:

- wait for the stock to return to 70 €, who asked for them in November 2019. Think, we will reach this level in the next 14 Months;

- wait for growth until 85 €. Given the company's gigantic dividend yield, it's not very rude. Think, we will reach this level in 3 of the year;

- hold shares 15 years and receive dividends.