DR Horton (NYSE: goat) - one of the largest American home builders. The company reported well, but what awaits her now and what distinguishes her from competitors for the better?

When creating the material, sources were used, inaccessible to users from the Russian Federation. We hope, Do you know, what to do.

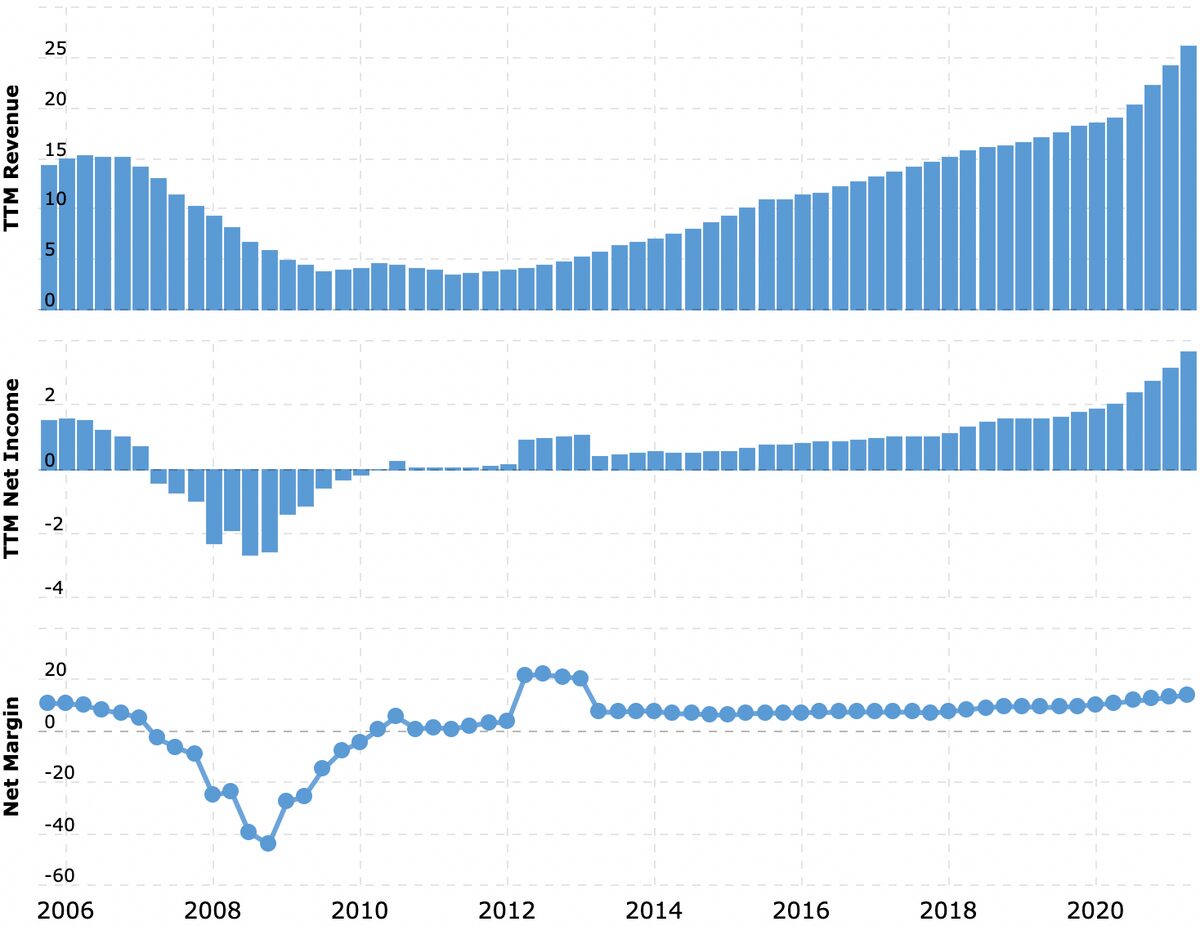

What do they earn

We did the analysis of the company's business back in 2020, so we won't repeat ourselves here., let's get to the point.

22 July, the company reported for 3 quarter - and the result was good: revenue increased by 35%, and profit - by 77%. Revenue increased in all segments: in the sale of houses, rent and finance. Tangible revenue growth took place in all regions.

Everything seems to be cool, but there is a nuance. If you delve into the reporting of the company, then you can see, that the total number of homes sold has fallen compared to the same period 2020, and strongly - on 17%.

The growth in revenue was due to an increase in the average price of houses by 22%. That is, the margin of home sales has increased significantly, despite the fact that the number of houses sold has fallen.

Let's look at the economic statistics - it came out a month after the report and reflects the situation, which shareholders of the company will have to face when reading the next report.

The real estate market has become unfriendly to buyers

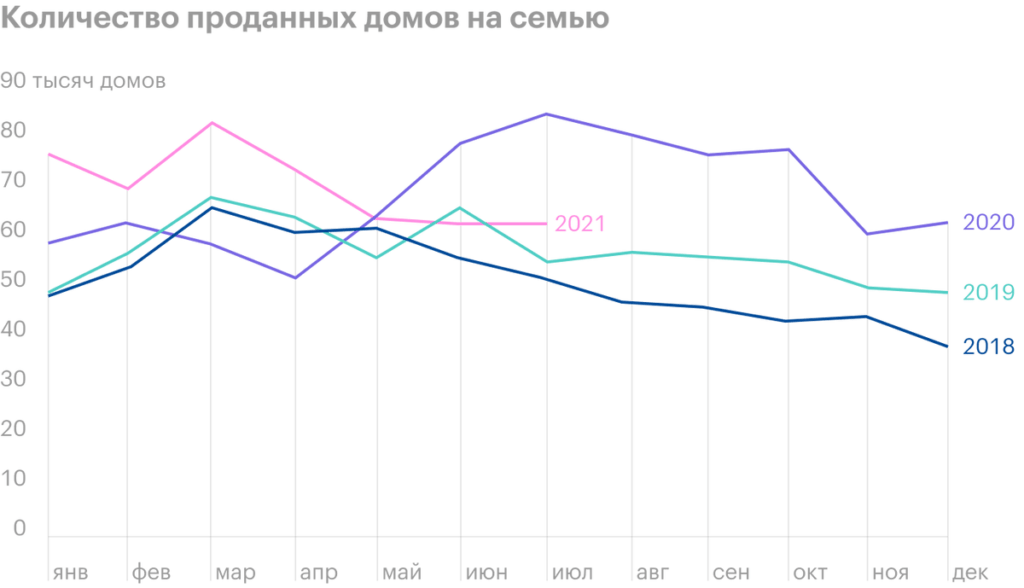

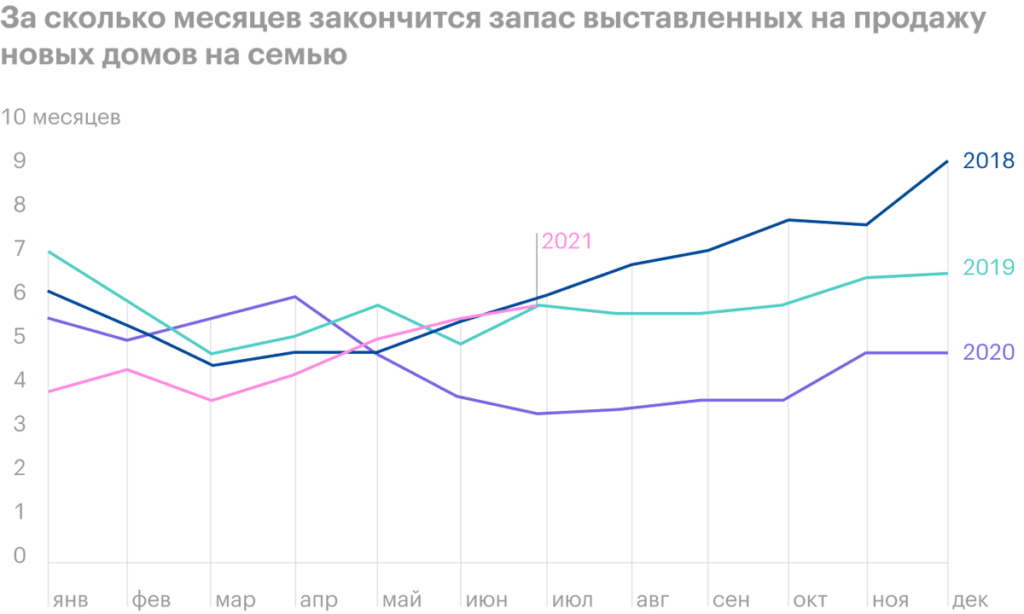

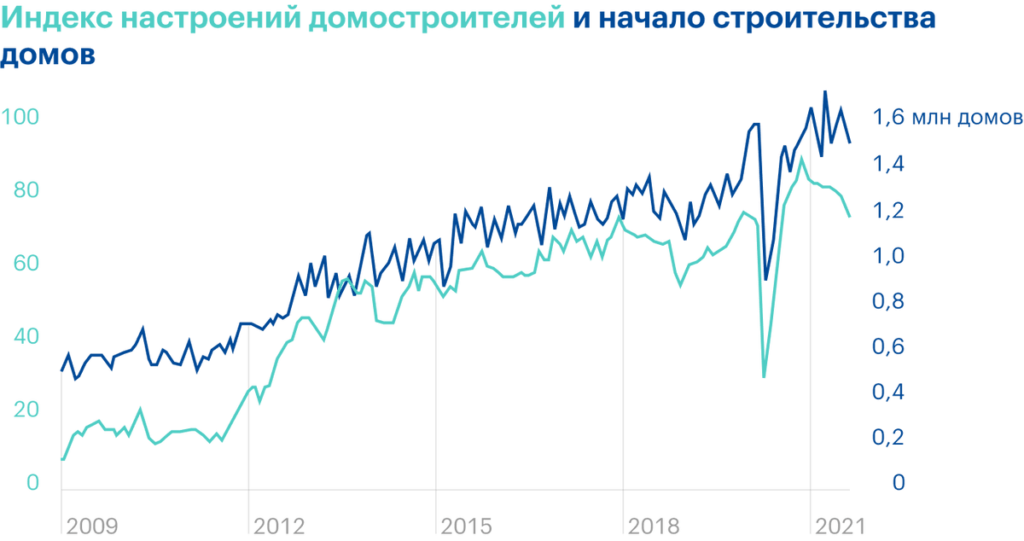

At first sight, American construction companies are now lucky: construction activity is at its highest for many years and companies are selling well even at home, which have not yet begun to build. This indicates high demand..

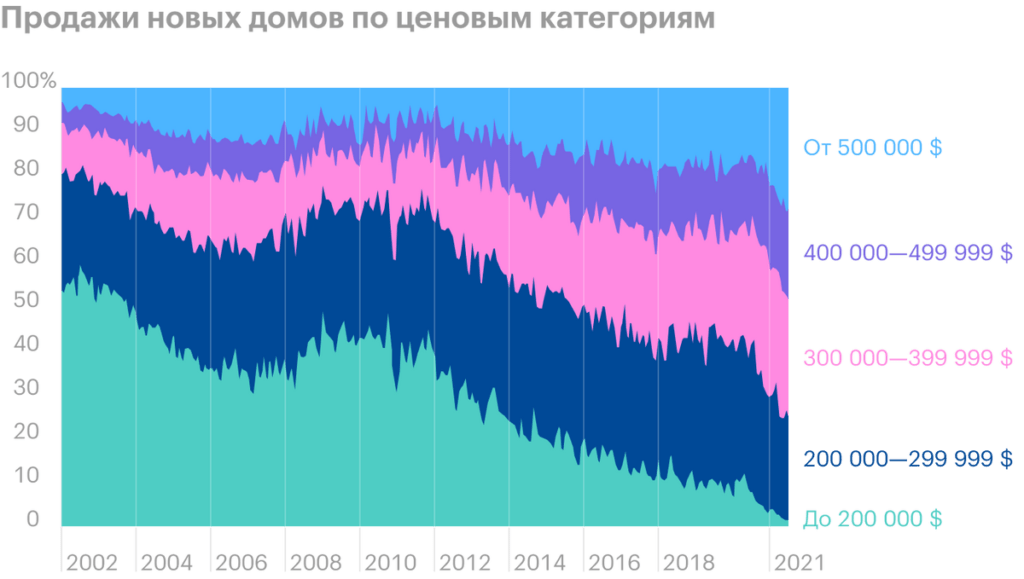

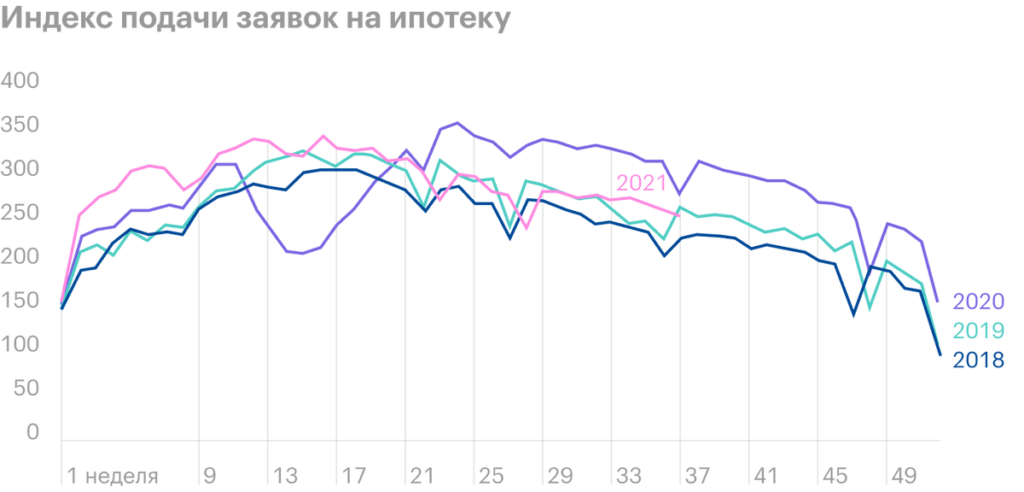

But when compared with 2020, then home sales have already started to fall, while the market supply increases, and this will significantly affect the prices of houses. In the structure of sold houses, real estate with a price much higher than the average plays an increasing role - which logically led to a fall in applications for mortgages.

All these processes are already affecting the mood of home builders., and therefore one should be wary of a decline in the financial performance of DR Horton: Demand has decreased and supply has increased. Buyers will be motivated to wait for more homes at affordable prices..

Here, Really, it is worth making a reservation: it's not about a crushing fall, but simply about a significant slowdown in growth - since we have to compare with abnormally high rates 2020. A similar situation happened with manufacturers of food and household goods.: in 2 in the quarter of 2021, all of them performed worse, than in the same period 2020, because at the beginning of the pandemic, people were frenziedly active, and then demand returned to normal. Home is, certainly, not products, but here we may encounter a similar story.

Positive

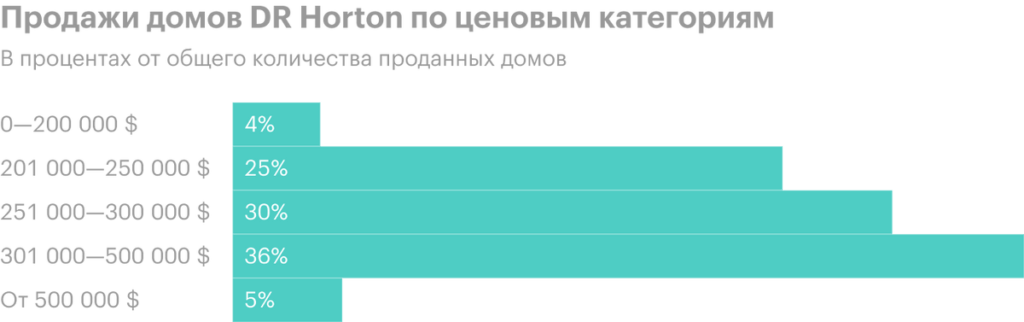

But let's not just talk about the negative - the company has pluses. Firstly, more than half of the homes sold by DR Horton are under $300,000, well below the median home price in the US, which is almost 375 thousand dollars. In conditions, when consumers become more price sensitive, it is important: means, the company's sales won't drop that much, as they could, in the event of a massive drop in demand in the real estate market.

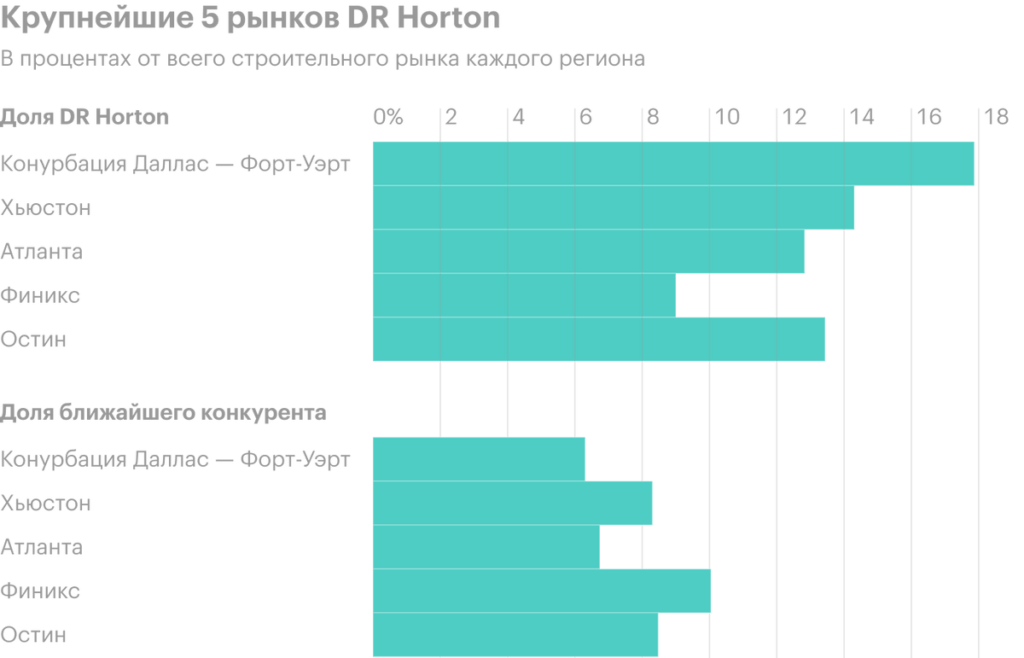

Secondly, the company holds a leading position in a number of promising regional real estate markets in the United States in the states of the South and Southwest. These markets were growing even before the pandemic thanks to the influx of new residents from the West and North.: for not very big money by the standards of New York and Los Angeles in the southern states you could find very decent housing with good surroundings.

But the combination of the pandemic and race riots led to a mass exodus of the solvent population from large agglomerations to the suburbs., and the digitalization of work has made it quite a working option with moving to another state, Cheaper. So the states of the South have become even more attractive in this context.. In the suburbs of the largest cities in Texas, Georgia and Arizona DR Horton takes the lead. Think, that these markets will become important growth points for the company's business in the future. Certainly, in the case of Texas, there is a constant threat of hurricanes and floods, but this is the cost of the profession.

The company is also benefiting from lower prices for wood, its main raw material.. Given the price range of her homes, this is an important point: the rise in raw material prices will not have to be factored into house prices. After all, if prices rise a lot, they can scare away the target audience of the company. This can be considered a plus, since the labor market will not be so merciful to the company - and the cost of labor, probably, will grow.

The cost issue is important because, what the company pays 80 dividend cents per share per year. On 0,91% annually takes about 288 million dollars a year. Although it is only 7,84% from the company's profits for the past 12 months and no apparent reason to cut payments. These reasons can appear very quickly., if the company's costs rise strongly. However, it is unlikely that DR Horton shareholders will sell shares in case of cuts in payments.

Resume

DR Horton looks like a very good option for that, to invest in the American construction industry. But here it is better to focus on the long term., to 5 years, and even more, because a lot can change in short distances. Demand for homes may fall, and the construction costs of the company can rise sharply. Over long periods, such troubles will not be felt so painfully., and the company will be able to realize its competitive advantages: relatively budget price plus dominance in the hottest regional markets.