Today we have a moderately speculative idea.: take shares of the German industrial enterprise Covestro (ETR: 1COV), in order to earn on the industrial rise in Europe and the world.

Growth potential and validity: 13,5% during 16 months excluding dividends; 8% per annum, taking into account dividends during 15 years.

Why stocks can go up: demand for the company's products will increase, the company is cheap.

How do we act: we take shares now by 56,34 €.

When creating the material, sources were used, inaccessible to users from the Russian Federation. We hope, Do you know, what to do.

No guarantees

Our reflections are based on the analysis of the company's business and the personal experience of our investors, but remember: not a fact, that the investment idea will work like this, as we expect. Everything, what we write, are forecasts and hypotheses, not a call to action. To rely on our reflections or not – it's up to you.

If you want to be the first to know, did the investment work?, subscribe: as soon as it becomes known, we will inform.

And what is there with the author's forecasts

Research, like this and this, talk about, that the accuracy of target price predictions is low. And that's ok: there are always too many surprises on the stock exchange and accurate forecasts are rarely realized. If the situation were reversed, then funds based on computer algorithms would show results better than people, but alas, they work worse.

So we're not trying to build complex models.. The profitability forecast in the article is the author's expectations. We specify this forecast for the landmark: as with the investment idea as a whole, readers decide for themselves, it is worth trusting the author and focusing on the forecast or not.

We love, appreciate,

Investment editorial office

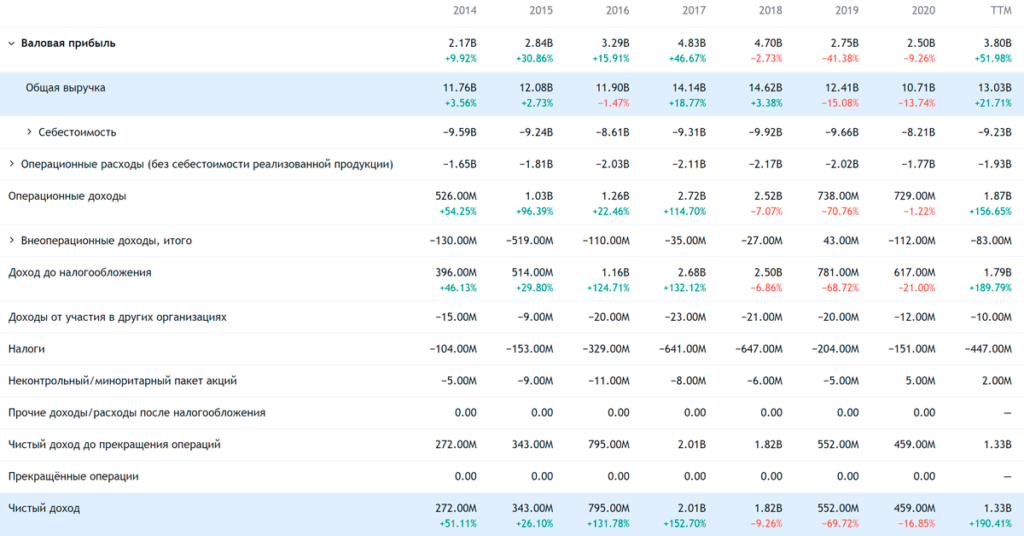

What the company makes money on

The company produces chemical materials, needed for the industry. According to the annual report, The company's revenue is divided as follows:

- Polyurethane — 47%. These are precursors for the production of rigid and soft foams.. Segment pre-tax profit margin - 3,92% from its proceeds.

- Polycarbonates - 28%. Materials for the production of high-performance plastics. Segment pre-tax profit margin - 11,12% from its proceeds.

- Cover, adhesives and special film-type solutions — 19%. Segment pre-tax profit margin - 10,54% from its proceeds.

- Other - 6%. These are by-products of the company's production such as hydrochloric acid.. Segment pre-tax profit margin - 3,17% from its proceeds.

The scope of the company's products is extremely wide - from all industries to construction and agriculture.

Revenue by country and region:

- Europe, Near East, Africa and Latin America without Mexico - 37,06%. Germany gives 10,81% of the entire revenue of the company.

- NAFTA countries - 20,57%. USA give 17,14% of the entire revenue of the company.

- Asia - 42,37%. China gives 18,12% of the entire revenue of the company.

Arguments in favor of the company

Demand. Industrial boom in most of the countries of the world, which was mentioned in the idea for Rheinmetall, is a big plus for the company.. So over the course of a quarter or two, you can hope for an improvement in her business..

Need more ESG. In its annual report, the company spends a lot of time, talking about various ESG metrics, up to the volume of carbon dioxide emissions into the atmosphere and the number of accidents at work. Certainly, An attentive reader may find fault with the methods of counting: for example, in the case of emissions, only those, that at the main plants of the company, not at all. But I think, that most socially concerned investors will not understand, and there are a lot of numbers in the report and everything is set up like this, that gives the impression of constantly improving the environmental friendliness and ethics of this business.

All this helps to create the image of Covestro as an ethical business - by inflating the company's quotes. Finally, Covestro presents a very beautiful picture of such a “responsible corporate giant” with continuous improvement in sustainability and business responsibility – and with a lot of numbers., which will take a lot of time for unfriendly experts to challenge. Considering, that ESG investing is now mainstream, you need to take this factor into account.

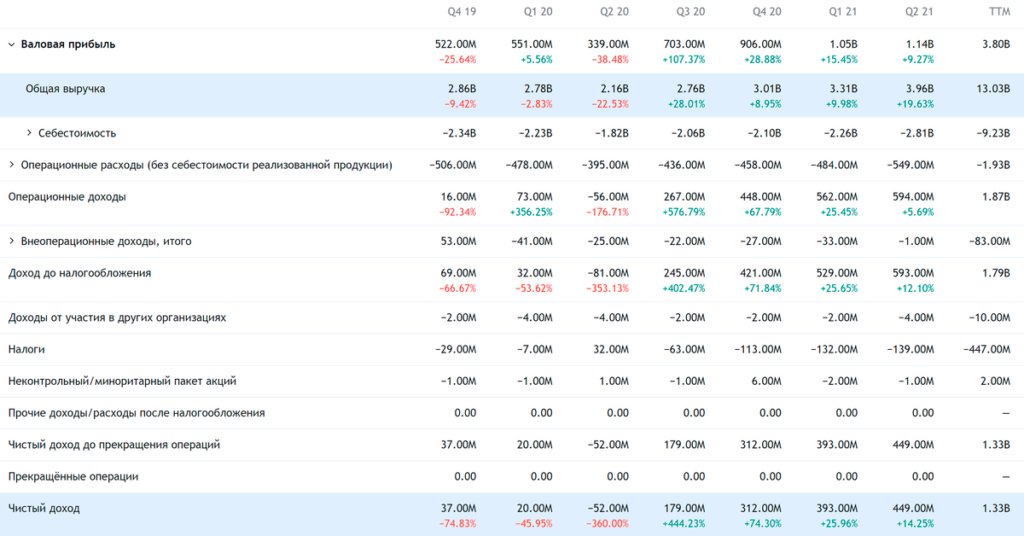

Inexpensive. Company P / E equal 8, a P / S she has 0,84. By all standards, especially American, the company is very cheap. This increases the chances of both an influx of investors into these stocks., which are of great interest to institutional investors, so and for that, that the company will receive an offer to purchase, most likely from overseas.

Wrecked. The company pays 1,3 € dividend per share per year - approx. 2,3% per annum. That's a lot by German standards - so I would expect, that Germans, exhausted by negative deposit rates, will swoop down on these stocks.

What can get in the way

"You give to the boy?» There is a risk that, that someone can arrange an audit of the company's financial statements in order to find inconsistencies in part of its ESG statements. In this case, the stock may fall sharply.. Moreover, this risk is permanent.

Prussian smell. Considering, that now in the world there is the strongest increase in the cost of logistics and a total shortage of everything - from equipment to raw materials, - you should mentally prepare for the growth of the company's expenses. Also, the “wild card” will be the situation with new strains of coronavirus: they can lead to a new "industrial pause" in the world, modeled on spring 2020, which will be a big blow to the Covestro business.

Mysterious China. In China, a slight decrease in industrial activity was recently recorded - this may be a sign that, that the company's sales specifically in China may suffer, what can be a problem for reporting. China accounts for almost ⅕ of Covestro sales.

Accounting. The company spends 257 million euros per year on dividends - less 20% from her profits for the past 12 Months. But Covestro profits are not always stable., and various force majeure events are possible, which could lead to cutbacks.

In the same time, according to the latest company report, it has approximately 8.058 billion euros of debt, of which 3.414 billion must be repaid during the year. The company doesn't have a lot of money.: 856 million on accounts and 2.266 billion debts of counterparties, although the company can scrape together the amount needed to pay off debts and pay dividends from other liquid assets. But there are still risks of cutting or even completely abolishing dividend payments., why the shares will fall. By the way,, payments at the beginning of the pandemic were cut in 2 Times.

What's the bottom line?

Shares can be taken now by 56,34 €. And then there are two ways:

- wait for the share price to rise to 64 €. Think, we will reach this level in the next 16 months, taking into account all the positive aspects;

- hold shares 15 years and receive dividends.